The 2026 California Guide: 10 Questions Every Family Must Ask Before Buying Life Insurance or Annuities

The world has changed. Inflation in California is higher than the national average, and the "old rules" of financial planning don't apply anymore. If you’re feeling the pressure of debt, a zero-savings balance, or the fear of a 2026 market crash, these are the 10 questions you need to answer.

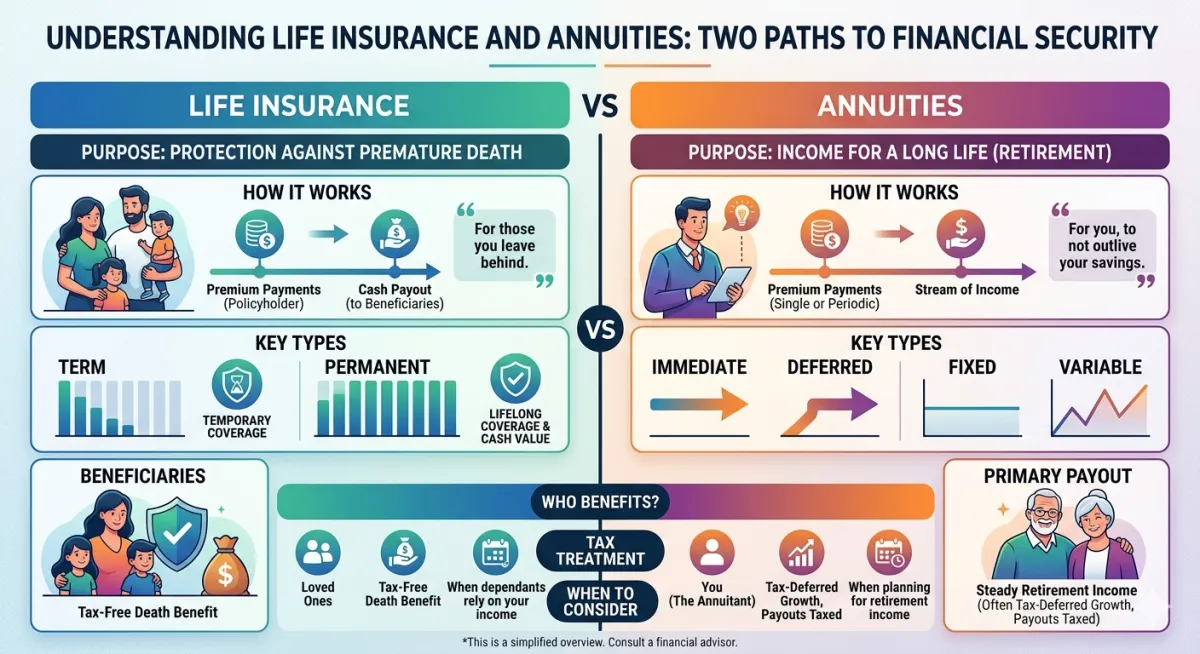

1. Is the "10x My Salary" rule still enough?

The Truth: No. In 2026, with housing costs and California's cost of living, 10x your salary is often a "poverty trap" for your family. We use the D.I.M.E. Method (Debt, Income, Mortgage, Education) to calculate a number that actually lets your wife and kids stay in their home, not just "get by" for a few years.

2. Why should I buy a private policy if I have "free" coverage at work?

The Truth: Work coverage is like a "rented" house; if you lose your job or get too sick to work, you're evicted from your policy. A private Elios policy is a "home you own." It follows you everywhere, regardless of your employer.

3. I heard IULs are a scam. What’s the catch?

The Truth: IULs aren't a scam, but they are often mis-sold. Many agents show you "dream illustrations" of 7% returns. At Elios, we show you the "Stress Test"—what happens if the market stays flat? You need an IUL for the Downside Protection, not just the upside potential.

4. What is the "$8,000–$15,000 Gap" I keep hearing about?

The Truth: That is the average cost of a funeral in California right now. If you don't have a specific "Final Expense" policy, that entire bill hits your family’s credit cards within 48 hours of your passing. Our 2026 plans lock in your rate so that bill is handled.

5. Can I get coverage without a needle or a medical exam?

The Truth: Yes. Over 50% of people avoid life insurance because they fear the doctor's office. In 2026, we use No-Exam Simplified Issue plans that use your data (not your blood) to approve you in minutes.

6. What happens to an annuity if the market crashes next month?

The Truth: If you have a Fixed Indexed Annuity, the answer is: Nothing. Your principal is protected by a "Floor." You get to participate in the market's gains, but the insurance company absorbs the losses. It’s "Longevity Insurance" for your 401(k).

7. Does the insurance company "keep my money" when I die with an annuity?

The Truth: Only if you choose a "Life Only" payout. Modern annuities have Death Benefit Riders and "Period Certain" options that ensure your kids or spouse receive every penny of the remaining principal.

8. Is "Whole Life" too expensive for someone with high debt?

The Truth: If you are carrying $100k in debt, you need Term Life with Living Benefits. It’s much cheaper and gives you a massive payout if you suffer a heart attack or stroke, allowing you to pay off that debt while you are still alive.

9. When is the "wrong" time to buy an annuity?

The Truth: If you need that cash for an emergency next week, don't buy an annuity. They are designed for Income You Can't Outlive. If you have zero savings, we focus on your "Protective Fortress" (Life Insurance) first, then build your "Income Floor" (Annuities).

10. How do I know I’m not overpaying?

The Truth: California is highly regulated. By using an independent agency like Elios, we shop the entire 2026 market to find the carrier that favors your specific health profile. We don't work for the insurance company; we work for your three kids.