Will Your Money Last as Long as You Do? The Longevity Risk Most Retirees Ignore

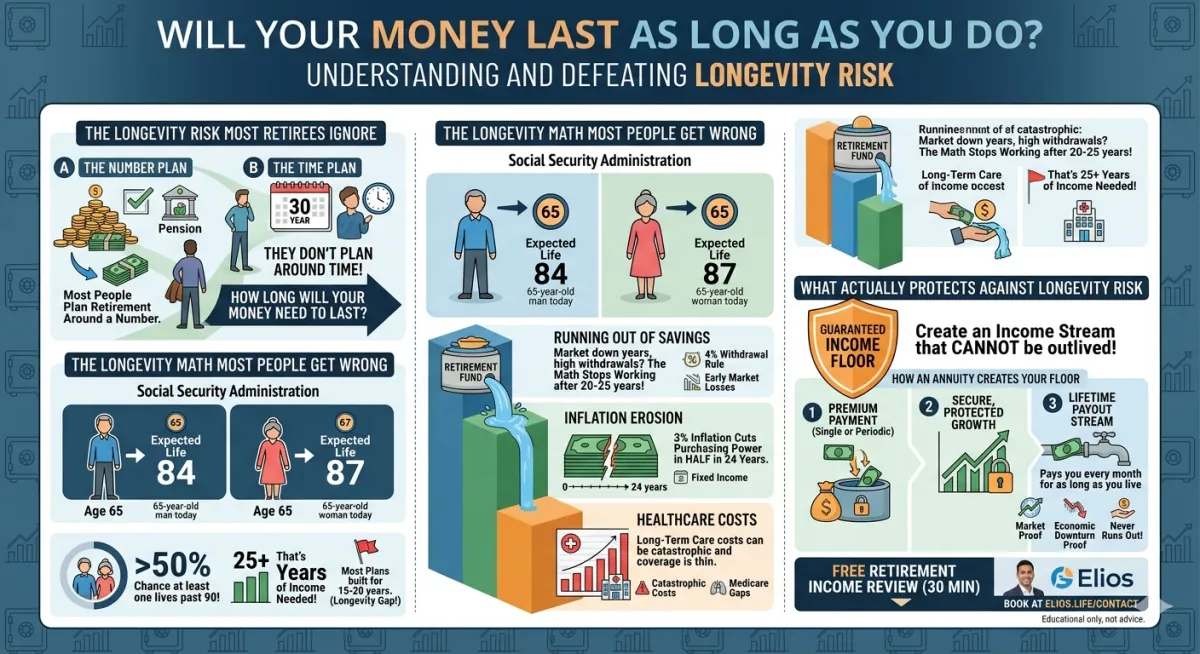

Most people plan their retirement around a number. A savings balance. A monthly Social Security check. Maybe a pension.

What they don't plan around is time.

Here's the question that should be at the center of every retirement plan — and rarely is: How long will your money need to last?

The Longevity Math Most People Get Wrong

According to Social Security Administration data, a 65-year-old man today can expect to live to age 84. A 65-year-old woman, to age 87. And if you're married? There's a greater than 50% chance that at least one of you will live past 90.

That's 25 years of retirement income to fund.

Most retirement plans — even well-designed ones — are built for 15 to 20 years. That gap between what's planned and what's actually needed is what we call longevity risk — and it's one of the most dangerous and most overlooked risks in retirement planning.

Why This Risk Is Bigger Than Most People Realize

Here's the problem: we tend to underestimate our own longevity.

Ask most 65-year-olds how long they expect to live, and they'll give you a number that's significantly lower than what actuarial data suggests. We think about our parents, our grandparents, our own health challenges — and we underestimate.

But healthcare advances over the past 30 years have quietly extended life expectancy in ways that most people's retirement plans haven't kept up with.

Living to 90 is no longer unusual. Living to 95 is increasingly common. And if you reach 90 in good health — statistically, you have a meaningful chance of reaching 100.

The question isn't whether you'll live that long. The question is: will your income keep up?

The Three Ways Longevity Risk Destroys Retirement Plans

1. Running Out of Savings This is the obvious one. If you withdraw 4% of your portfolio annually and your portfolio grows at a modest rate, you might be fine for 20 years. But at year 25 or 30? The math stops working — especially if markets had a bad run early in your retirement.

2. Inflation Erosion Even modest inflation at 3% per year cuts the purchasing power of a fixed income in half over 24 years. If your income stays flat but your expenses keep rising, you're effectively taking a pay cut every single year.

3. Healthcare Costs The longer you live, the more likely you are to face significant healthcare expenses. Medicare covers a lot — but not everything. Long-term care, in particular, is a category where costs can be catastrophic and coverage is thin.

What Actually Protects Against Longevity Risk

The most effective protection against outliving your money is creating an income stream that cannot be outlived — one that pays you every month for as long as you live, regardless of how long that turns out to be.

This is exactly what certain annuity products are designed to do.

A properly structured annuity can create what we call a guaranteed income floor — a base level of monthly income that continues no matter what. Market crashes don't touch it. Economic downturns don't affect it. And it doesn't run out at year 20 or year 25 or year 30.

It simply continues. For life.

A Note On Planning Realistically

I want to be clear about something: not every retiree needs an annuity. And an annuity is rarely the right choice for 100% of someone's assets.

But for retirees who are worried about outliving their money — which, in my experience, is most of them — having a guaranteed income floor that covers essential expenses can be genuinely life-changing. Not just financially, but psychologically.

The retirees I work with who have a guaranteed income floor tend to sleep better. They spend more freely on the things that matter to them. They worry less about market swings. Because regardless of what happens, the essential bills are covered.

The Free Retirement Income Review

If you're 65 or older and you've wondered whether your retirement plan is built to last as long as you do — that's exactly the question a free Retirement Income Review is designed to answer.

In 30 minutes, we'll look at your current income sources, your expenses, and the gap — if there is one. Then we'll discuss whether a guaranteed income floor makes sense for your situation and what that might look like in real numbers.

No obligation. No pressure. Just clarity.

[Book your free review at elios.life/contact]

Siraj is the founder of Elios Insurance Agency and an IRS Enrolled Agent with 20+ years of accounting and finance experience. Elios Insurance Agency serves retirees 65+ in Southern California.

Insurance products and their features vary by carrier and state. This article is for educational purposes only and does not constitute financial or insurance advice. Please consult a licensed professional regarding your specific situation.